The Hire Purchase (Amendment) Act 2026: The End of “Flat Rate” Car Loans

The government just passed the Hire Purchase (Amendment) Act 2026, and with it, they killed the Rule of 78.

Here are the key changes:

- No more Rule of 78 calculation method for early settlement.

- No more flat interest rate structure.

- All hire purchase loan shifts over to a reducing balance method alongside the Effective Interest Rate (EIR), which means you finally get to know the true cost of financing.

In plain English: the “flat rate” car loan is dead.

I’ve always hated flat rates. They’re designed to confuse people by creating the illusion of a low interest rate. Getting rid of them is one of the best things the current administration has done for consumer transparency.

If you’re planning to buy a car anytime soon, this directly affects you. I’ve been digging through the details of the new Act, and here is what it actually changes on the ground.

Why the “Flat Rate” Was Deceptive

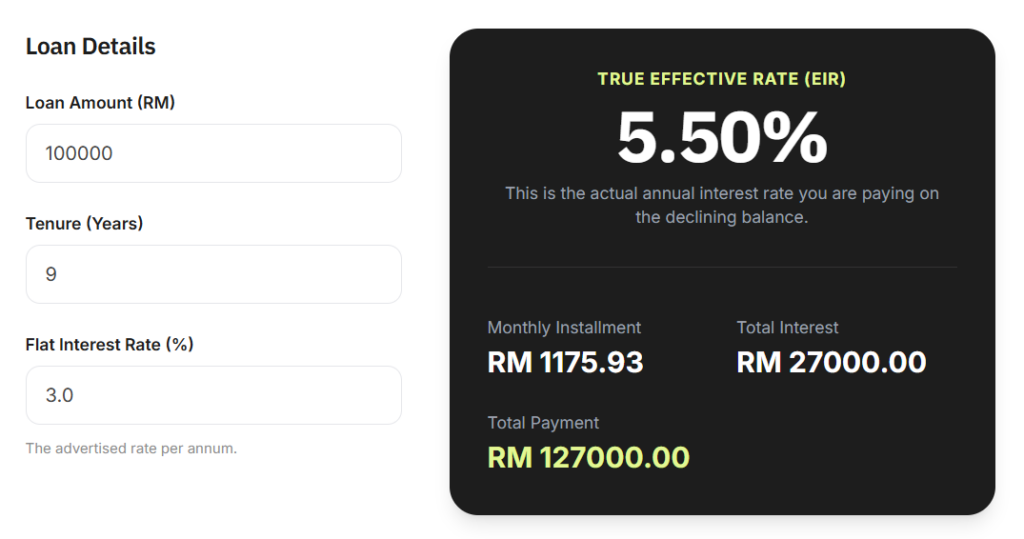

Say you take a typical 9 year car loan. The bank quotes you 3% p.a.

You see 3% and assume it’s cheaper than your 4% mortgage. It’s not.

Under the old flat rate system, interest is calculated upfront on the original loan amount. You don’t get any break on interest as your balance drops over the years.

Worse, those interest payments are heavily front loaded. Anyone who has tried to settle their car loan early knows the pain, you go to the bank after three years of payments, only to find out you’ve barely touched the principal. All your money went to interest. The system actively punished people trying to clear their debt.

If you’re stuck in one of these old loans and want to see the real numbers, I built a Flat Rate to Effective Interest Rate Calculator you can use.

Does this mean car loans are now cheaper?

Maybe. Probably not.

The new Act forces banks to use the reducing balance method and show you the Effective Interest Rate (EIR). We finally get transparency, but transparency doesn’t magically make borrowing cheaper.

A standard 9 year loan with a 3% flat rate actually translates to an EIR of about 5.5%.

When the law kicks in on June, banks will quote the EIR upfront. If the new rates they offer are significantly lower than 5.5%, then yes, consumers win. But if banks just swap the sign and quote you a 5.5% EIR, you’ll be paying the exact same amount of interest as before. You just won’t be lied to about it.

(Side note: From what I’ve read, this law isn’t retroactive. If you already have a car loan, your monthly repayment isn’t going to change.)

Does this mean you should pay off car early?

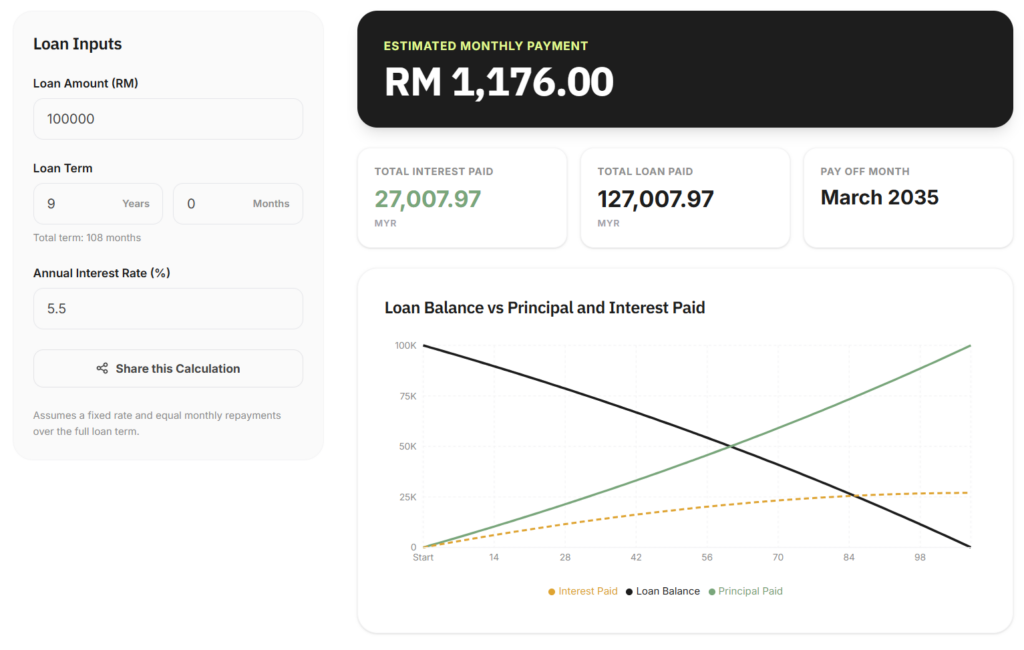

The main benefit of the new reducing balance method is that settling early actually works. Since interest will be calculated monthly on your remaining balance (just like a housing loan), throwing extra cash at your car payment directly reduces your principal.

If you want to model this out, you can use my Amortized Loan Calculator.

But personally? I’m still paying the minimum on my car.

Even at a 5.5% EIR, I’d rather deploy my cash elsewhere. For example, a diversified market index funds are consistently returning above 10%, dumping extra money into a 5.5% loan is a bad trade. I’ll let the cash compound in the market.

However, If you hate having debt hanging over your head, clearing the loan is perfectly fine, but at least know what is the opportunity cost.

The remaining problem

Forcing banks to use effective interest rate for car loans is a solid win. I just hope it doesn’t stop here.

Hiding the true cost of debt is practically an industry standard. Just look at Buy Now Pay Later (BNPL) scheme offer by various platform they still mask their insane interest rates behind flat fees and confusing terms. Personal loan marketing isn’t much better, frequently burying the real EIR in the fine print.

Killing the car loan flat rate fixes a massive blind spot in Malaysian personal finance. Now the authorities need to go after everyone else doing the exact same thing. The goal is to have only standardize fair interest rate based on actual capital borrowed and balance amount.

Should also forbid banks or financial services to run promo or “fake rewards” at insane high rate, for example “Up to 10% cashback!” then in fine print “for the first rm100”, these are all deceptive marketing in my opinion.

Now I’m curious to hear your thoughts, when banks finally start displaying the true effective interest rate upfront, will it make you think twice before signing that 9 year car loan? Let me know in the comments!

Comments