Best Air Miles Credit Card in Malaysia [Updated 2025]

![Best Air Miles Credit Card in Malaysia [Updated 2025]](/_next/image/?url=https%3A%2F%2Fmalaysianpf.com%2Fwp-content%2Fuploads%2F2024%2F05%2FBest-Credit-Card-for-Airline-Miles.png&w=3840&q=75)

This post has been updated for year 2025, benefits of some cards has been revised by banks, and some cards with campaign has been expired and discontinued. I recommend to check back this post at least once a year to decide the best cards to use throughout the year for maximum potential.

What Is The Cash Value of Air Miles?

Air miles credit cards are often considered the pinnacle of credit card strategies, offering significantly greater savings potential compared to cashback cards or other credit card types.

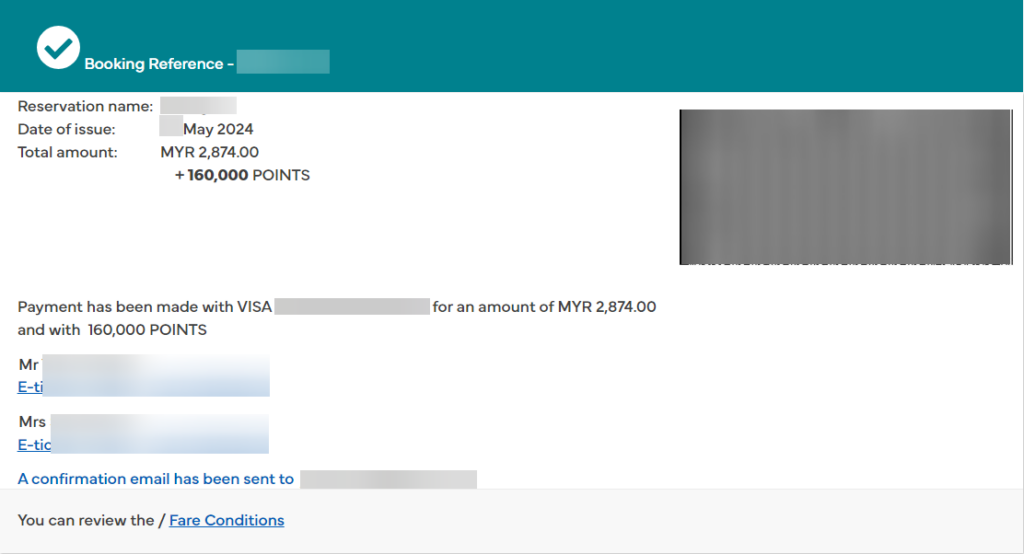

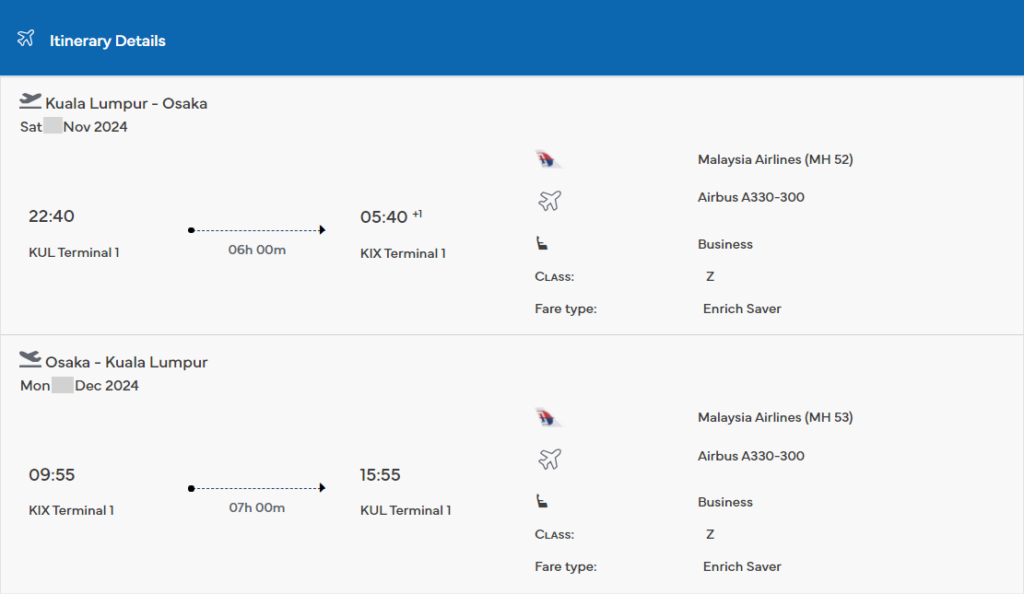

For instance, I recently booked another business class flight to Japan for the upcoming autumn season with my spouse. The total cost amounted to RM 2,874, along with redeeming 160,000 Enrich points for two round-trip flight tickets.

To calculate the return of ringgit spent (ROI) on this booking, we’ll start by determining the average cost of booking a business class flight ticket to Japan without using air miles. Then, we’ll conduct a reverse calculation to find out your ROI.

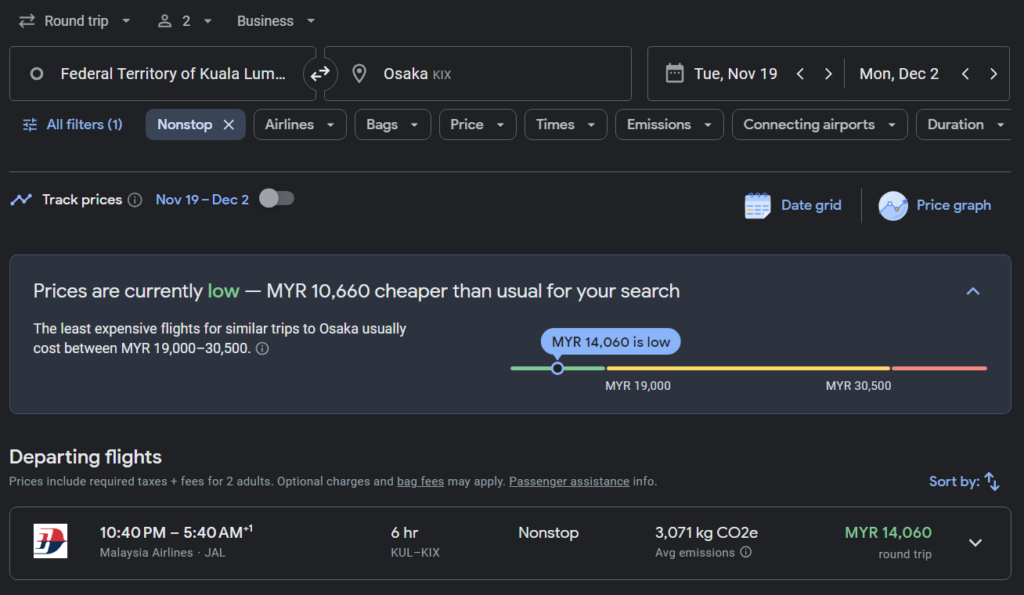

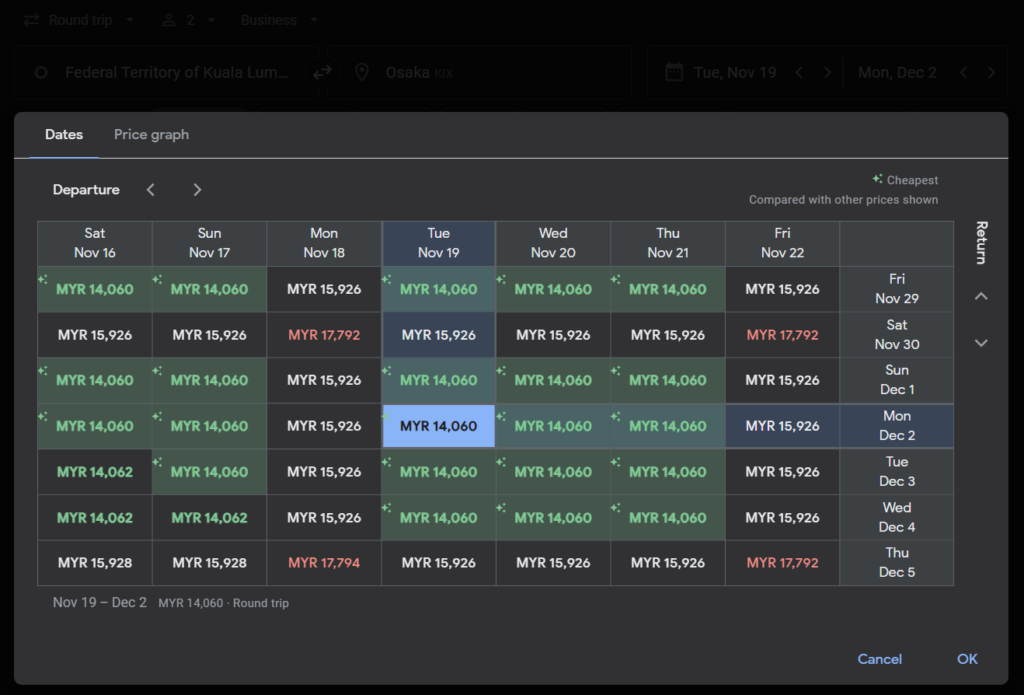

First, let’s utilize Google Flights to gauge the typical cost for this flight. We’ll ensure we’re not selecting the most expensive date to avoid skewing the calculations.

From the above screenshots, it’s evident that our flight fares are lower than usual, which is advantageous and ensures a more conservative approach for our calculation. Opting for a less expensive date guards against bias toward the benefits of air miles credit cards, as it means our air miles are worth their typical value rather than inflated due to higher-than-average flight costs.

Let’s proceed with the calculation. We’ll determine the value of each air mile by subtracting the cash paid from the regular ticket price, then dividing the result by the number of air miles redeemed.

(RM14,060 - RM2,874) / 160,000 = 0.0699125Based on our calculation, the value per Enrich mile is approximately RM0.07. These miles are predominantly accumulated through the Alliance Bank Visa Infinite card, which provides approximately 0.8 air miles for every RM1 spent.

To calculate the return on spend (ROI) of this air miles credit card, we first determine the cash value of 0.8 air miles by multiplying (0.8 * RM0.07), resulting in RM0.056 for every RM1 spent. This equates to a 5.6% return on ringgit spend (ROI).

Isn’t that an incredibly impressive return on ringgit spent (ROI)?

Additionally, it’s worth noting that a significant portion of my air miles were redeemed during promotional periods with a 20% bonus offered by Malaysia Airlines on occasion. This bonus further enhances the overall value proposition of utilizing air miles credit cards.

Best Airmiles Credit Card in Malaysia

Before determining the best air miles credit card for our needs, there are several crucial metrics and factors to consider, such as:

- MPR: Miles you will earned per every ringgit spent, usually higher is better

- ROI / RM1 Spent: Similar to MPR, but we assign a value of 0.04/miles to calculate the nominal ROI value, so that it can be compared to non-airmiles card

- Airline Options: Usually you will want to earn miles from airline that you’ll actually use

- Annual Fees: This are cost that you should consider in the calculation, as it will directly lower the ROI of your card

- Salary Requirement: Helps you to understand if you are eligible to apply for this card, some times this is also the amount of deposit needed if you apply card with fixed deposit collateral

Other factors that are also important includes:

- The foreign transaction fees, most bank charge 1% on top of the visa/master exchange rate, which means in real world the exchange fees are usually about ~2% on top of mid market exchange rate. (Maybank AMEX 2.5% includes both, so you’ll expect ~2.5% on top of mid market exchange rate).

- The limit of lounge access, most bank will publish a list of lounge that you’ll be able to access with your card, but because it’s less important in my opinion, so I’ll just count all lounge access equal regardless which airport they are limited to.

- Qualified spending categories, most card focus on physical in-store spending, while some are better for online spending. Some for frequent foreign currency spending, and some for your local day to day spending.

- Monthly capping and merchant capping is another thing you should be aware of, usually I prefer to recommend card with least capping even if that means lower ROI, unless the capping are well above your spending. (In our opinion the point of improving our personal finance is to make life easier, and having to keep track of the capping of each card goes against that very purpose.)

Here I’ve made a table based on above metrics and factors, some of them have more complicated rules, especially for qualified spending categories and capping, however this table is made for generic spending pattern. (ie: I do not want to think about which card to use every time at cashier while 10 people waiting in the line.)

⚡ View full table with filterable options to help find your ideal credit cards here.

*For Visa & Master Card the foreign exchange fees are the one imposed by bank, it doesn’t include network fees which is typically another 1%.

**For AMEX Card the foreign exchange fees included the fees imposed by bank and network fees.

My Top 3 Air Miles Card Recommendation

1. Standard Chartered Journey Credit Card

If your staying abroad most of the time or travel frequently, with a salary of at least RM8000 per month, then this is currently the credit card with highest miles per every ringgit spent at 1 miles per every ringgit.

The annual fees is RM600 per year but it is free for the first year and it will be waived automatically if you spend more RM60,000 per year, which might be easily achievable if you live or working abroad.

However if you spend less than RM30,000 per year on this card and has to pay annual fees, then this card is probably not worth for you, the first RM15,000 spent will just get you break even with the annual fees.

2. Alliance Bank Visa Virtual & Alliance Bank Visa Platinum

Many people cancelled their Alliance Bank credit cards since they revised their card benefits and added capping, but in my opinion the lower tier Visa Virtual and Visa Platinum are still a pretty good option for local ecommerce spending (Shopee / Lazada).

Both card have a capping of RM3000/month on ecommerce spending and ewallet topups, which means you will maxed out the potential after spending RM6000 on Shopee and topup RM6000 on ewallet for both card combined.

The Visa Platinum has an annual fees of RM120 but it will be waive automatically after using the card for 12 times in that year, which is easily achievable.

There’s no annual fees with the Visa Virtual and it’s an incredible card as it will let you create as many virtual cards you need with customizable spending limits and expiry date. This become especially useful for purchasing online from less reputable platform.

3. HLB Visa Infinite

This card is recommended because it has no annual fees for life, automatically redeem Enrich miles every month, 0.45 MPR on foreign currency spending and 0.28 MPR for local currency spending.

It also doesn’t have too much of merchant limits, both online and offline retail transaction will be eligible, except for the “cash advance” and FPX transactions.

The downside of this card is it only earns you Enrich miles, but that shouldn’t be a problem for most Malaysian.

Maximizing The Return from Airmiles Credit Card

Now that we’ve explored the value of air miles and identified the top credit cards in Malaysia for accumulating them, did you know there are additional ways to maximize the return of your air miles credit card?

Essentially, maximizing the return of your air miles credit card involves paying close attention to ongoing promotion campaigns from both your credit card bank and the airlines from which you want to earn air miles.

Here’s an example of how you can capitalize on flight booking promotions with Enrich miles on Malaysia Airlines: during the promotion period, you can enjoy a 20% discount on air miles when booking a flight. By leveraging this promotion, we were able to book our flight to Japan and maximize our savings.

Another example of maximizing your air miles is through past promotion campaigns by Malaysia Airlines. For instance, they offered a promotion where you could receive a bonus of 10-20% Enrich miles by converting your credit card points into air miles during the promotional period. This is another opportunity to boost your air miles balance and increase your redemption options.

Here’s a quick calculation: by taking advantage of both promotions, you’re effectively getting up to 50% more value in terms of miles per ringgit spent.

[100% * 120% (Points Conversion Promo)] / 80% (Booking Discount Promo) = 150%If you’re a frequent flyer with Malaysia Airlines, keep an eye out for their promotions in your email inbox or on their website: https://enrich.malaysiaairlines.com/enrich/promotions.html

What About Other Credit Cards? Missing Info?

I try my best to keep this post up to date but as a human I may still missed out on some credit cards, or maybe revision from some banks affecting certain cards miles per ringgit, but don’t worry, if you think I missed out on some card should be listed here, or information that are outdated, just leave a comment and I’ll look into it!

Comments