The Ultimate Guide to Using 0% Balance Transfers for Investment

What Is Balance Transfer

Balance transfer is a service that often comes with your credit cards. As the name suggests, it’s a service that transfers the outstanding balance from one credit card to another.

In most cases, the balance will be converted into monthly installments. Many credit card holders overlook this service, assuming it’s only for those struggling to pay their monthly statements.

However, the strategy I am about to share is way beyond that. When used correctly, it can greatly accelerate your financial growth.

The 0% Balance Transfer Campaign

This is the main criteria we need for our balance transfer strategy to work. Let me tell you this, banks often run 0 interest balance transfer campaigns from time to time. You just need to be aware and pay attention to them.

0% interest on a balance transfer literally means the bank is giving you a no interest loan. This means whatever amount you were about to pay to your credit card statement can be used to invest into something else. You earn interest on that cash, then slowly pay back the principal.

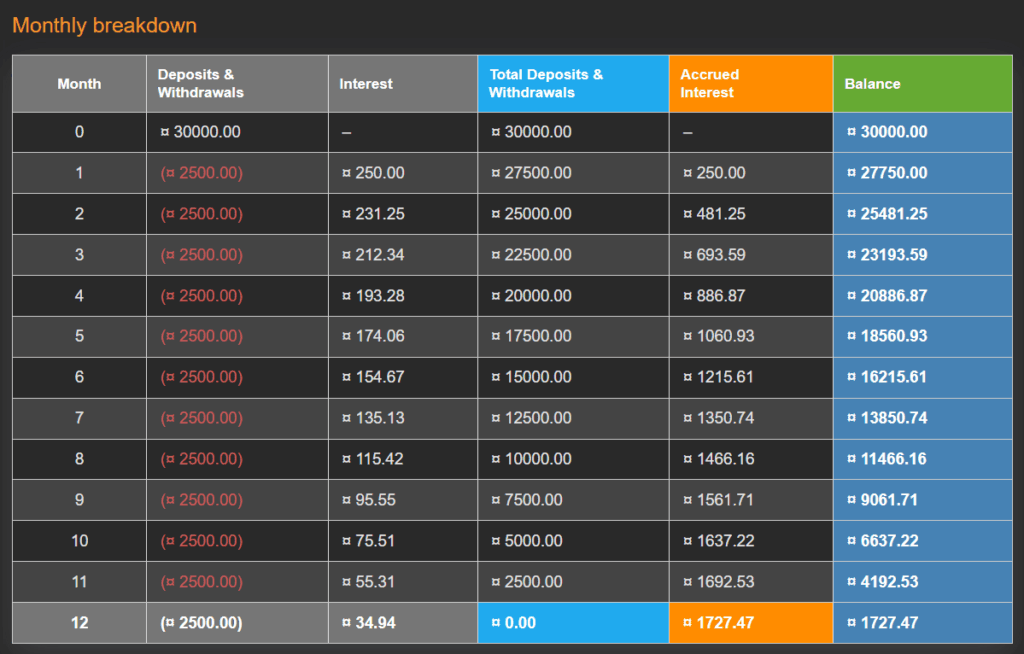

Here’s an illustration of how that works. Assume you owe RM30,000 on a credit card statement. You take advantage of a 0 balance transfer campaign. Now, you are required to pay a RM2,500 installment for 12 months. Instead of paying the RM30,000 upfront, you put it into an investment and withdraw from it monthly.

By the time you pay the last installment, you would end up with RM1,727 (assuming an annual profit rate of 10%). This is profit you wouldn’t have if you just paid the RM30,000 statement in full without the balance transfer!

Before You Jump Into Conclusion

Whenever I share this strategy, people often raise objections like, ‘What if the investment fails?’ or ‘It’s not worth the effort.’ For those who can comfortably spend RM30k, the potential profit might seem small.

Without wasting your time, I will start with the conclusion: this strategy scales immensely over the long term. If you are interested to learn how to compound this, read along.

The Strategy: Chaining Balance Transfers Indefinitely

Here is the really exciting part: what if we chain all the balance transfer campaigns together?

Based on the previous example, we were supposed to withdraw RM2,500 to pay the installment. But what if you pay that RM2,500 with another balance transfer credit card? And keep doing that for the following months?

It’s simple, you wouldn’t need to withdraw any of the RM2,500. Those funds continue to stay in whatever investment vehicle you chose, earning profit or interest.

Rolling That Interest Free Loan

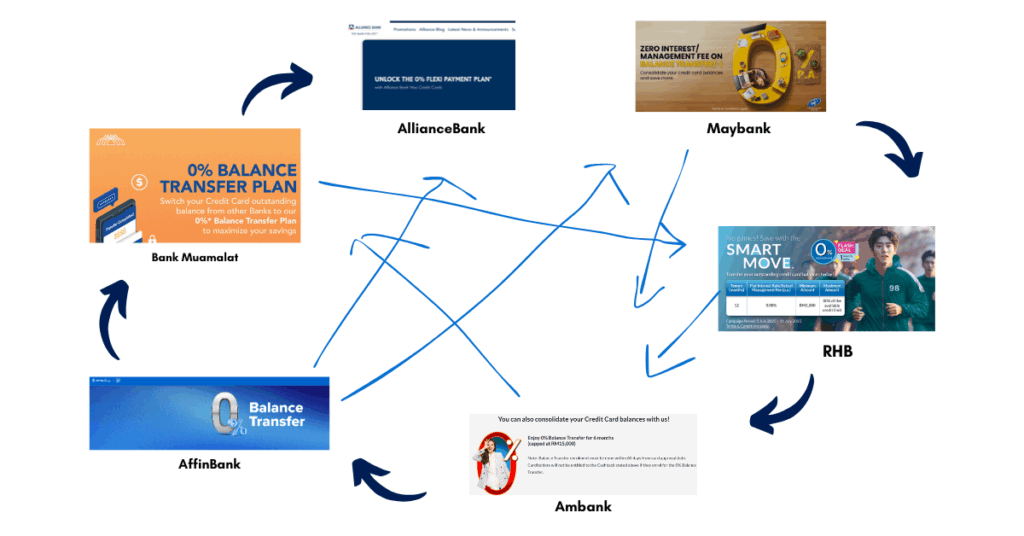

When you have credit cards from multiple banks in Malaysia (like Maybank, CIMB, or Alliance) and apply this strategy long enough, you will eventually saturate up to 60~80% of your available limits.

To fully utilize this interest free loan, just put all your regular living expenses onto the card. As you roll the loan by continuously taking up 0% interest balance transfer campaigns, your credit limit will eventually be saturated with 0% money.

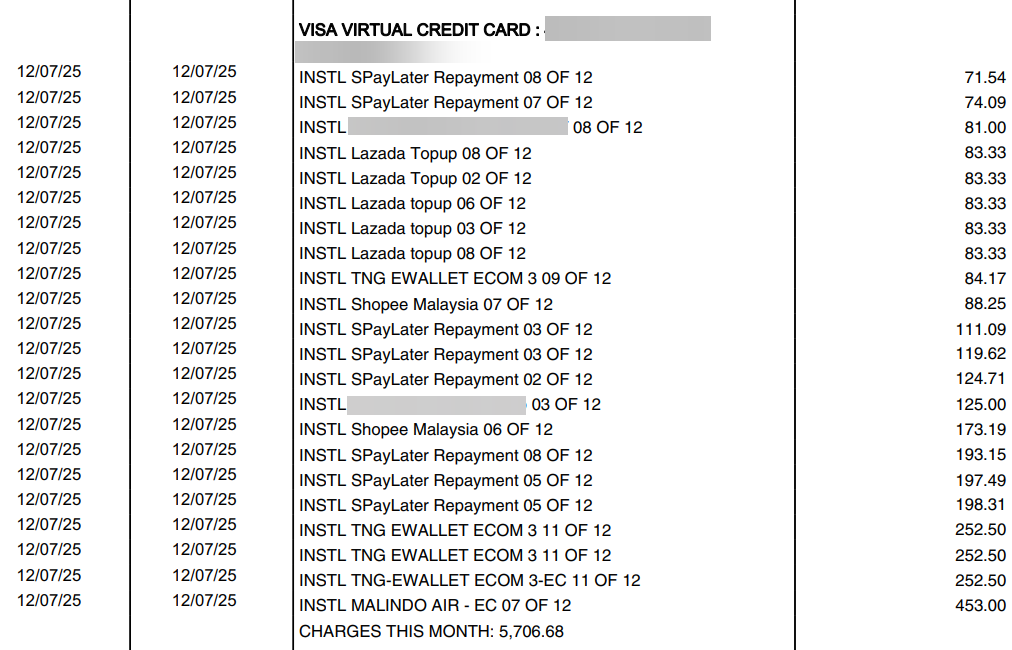

This is what my statement looks like with those balance transfer items:

Other 0% Interest Loans from Cards

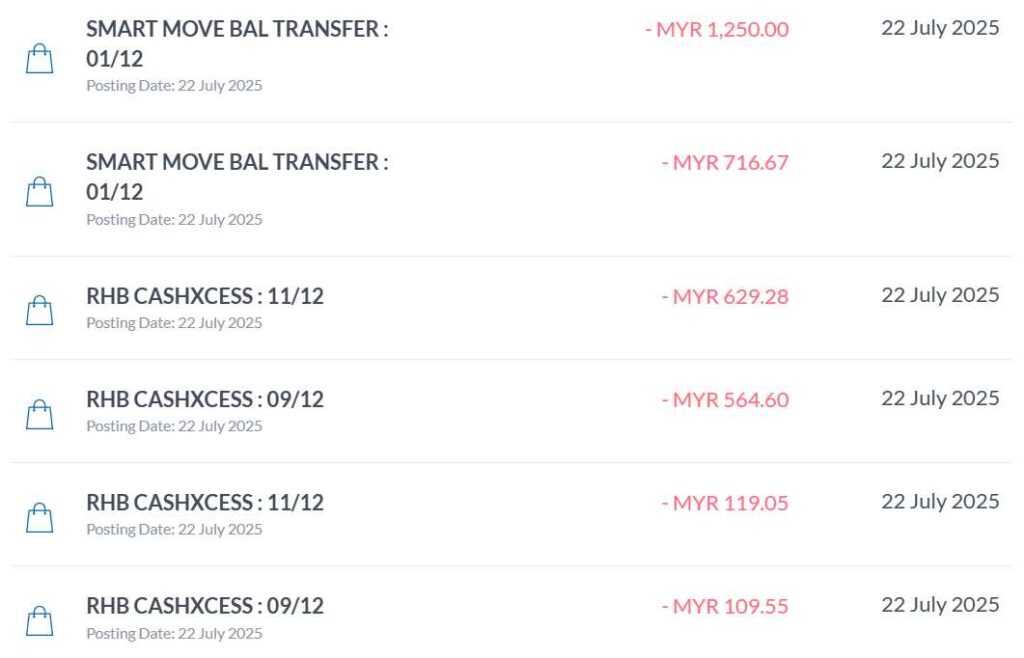

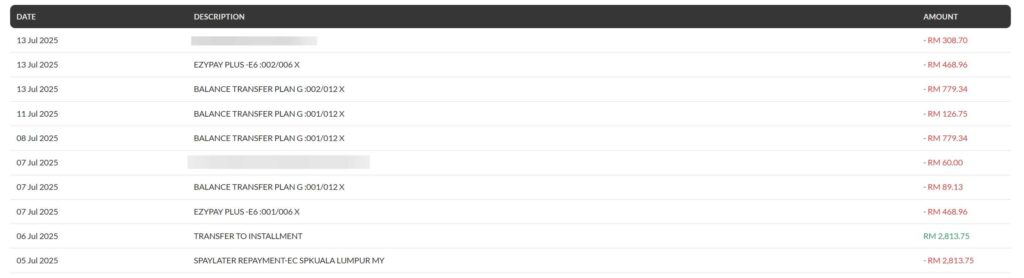

Now, for those with sharp eyes, you’ll see that the items on my Alliance Bank Visa Virtual are not technically “balance transfers.” Some items on my RHB are not balance transfers too!

That’s right, but they serve the exact same purpose. They extend the way you can put your regular living expenses onto your credit card to free up capital. Let me explain.

The Alliance Visa Virtual let me convert any transaction above RM500 into a 0% interest installment. That means the card itself allows me to utilize up to 100% of the credit limit Alliance Bank gave me.

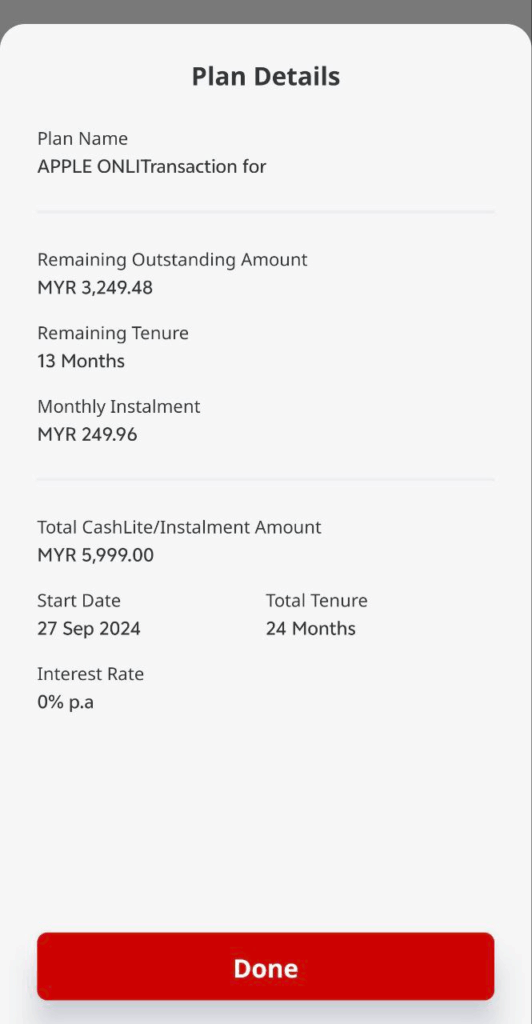

The RHB CashXcess was applied during their 0% campaign period, which let me cash out my credit card limit directly to my bank account, allowing me to cover expenses that aren’t even payable by credit card.

Sometimes, cards will run 0% EPP/FPP/IPP campaigns to let you convert transactions above a certain amount into 0% installments too.

For example, this was a 24 months balance transfer/installment campaign from CIMB last year that let me reply to an SMS to convert a transaction to a 0% installment.

All of these are essentially the same thing, a zero interest loan from the bank based on your credit limit. Whenever your monthly statement arrives, just pay that statement with another balance transfer campaign.

Keeping Track of All The Balance Transfer

One question I get asked often when sharing this strategy is: how the hell am I supposed to keep track of all these balance transfers?

The short answer is: You don’t.

You’ll check your credit card statement on the first of the month as usual. The only difference is that instead of paying the statement with cash from your checking account, you’ll apply for a balance transfer to pay it off. It’s that simple.

What if there are no 0% balance transfer campaigns that month? If there are absolutely no campaigns from any of the banks you use, then you just pay it with cash or withdraw from your investment. That’s it.

The Advantage of The Balance Transfer Strategy

Why do I say that when this strategy is used correctly, you can accelerate your financial growth? Let me illustrate with simple math.

Banks often give a credit card limit of 25~50% of your annual income. If you hold cards from multiple banks, your combined credit limit could easily hit 100~200% of your gross annual income. Personally, I have credit cards from 6 banks, and my combined limit is roughly 200% of my gross annual income.

Now, if I just utilize 50% of that, it means I took an interest free loan equal to 100% of my gross annual income. Those funds are invested and earning me interest every year.

How long does it take an average person to save up an amount equal to their gross annual income? Assuming you save 30% of your income after tax (and assuming average income tax at 15%), you can save 25.5% per year.

That means it takes 4 years to invest the same amount I got upfront from my 0 balance transfer credit cards.

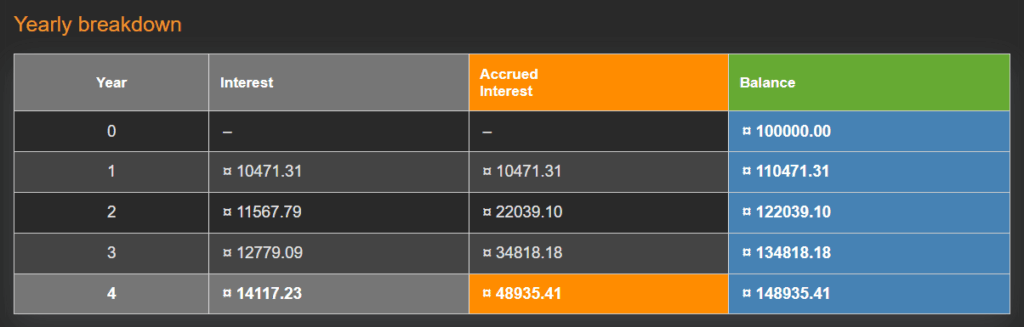

Let’s compare the difference. Assume an annual income of RM100k, invested into an index ETF at an average 10% per year.

Both invested RM100,000 cumulatively. But the guy who utilized the balance transfer strategy to “invest first, pay back later” ended up with RM149k instead of RM122k. That difference is significant!

But hold up. The strategy isn’t just about paying back later; it’s about chaining the balance transfers indefinitely. There is no reason for the first guy to pay off that RM100k outstanding if he can continue to roll it over with 0% interest loans.

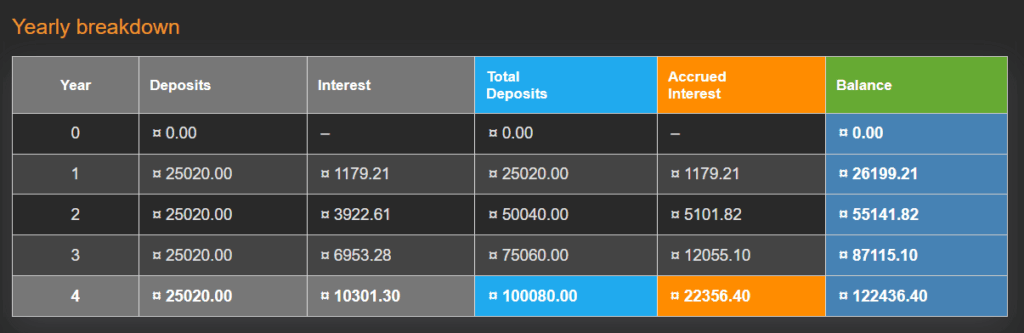

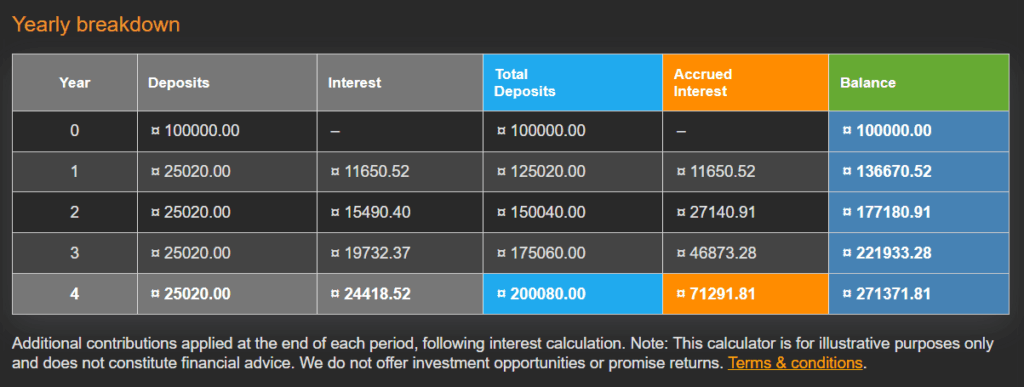

This means the first guy can also invest 30% of his net income on top of the strategy. Here is what happens over 4 years:

The first guy ends up with RM271k in his investment account. Even if he decides to suddenly clear the RM100k outstanding balance, he still ends up with RM171k net.

The Difference Is Even Mind Blowing in Long Term

I want to show you how the benefits from that early 4 years of “front running” turns into a massive structural advantage.

Assuming both maintain the same salary for the next 10 years. In 10 years, the first guy would end up with RM698k in his account. After deducting the RM100k outstanding loan, his net worth is RM598k. That is 40% more than the regular guy who only has RM427k.

In 20 years, the first guy ends up with RM2.216 million compared to the second guy’s RM1.58 million. The 40% difference remains, but the RM100k debt has turned into a relatively tiny percentage of the total net balance.

Wait, But Investment Is Not Guaranteed?

That’s right, investment returns are not guaranteed and won’t be perfectly linear. However, that actually favors the guy using the strategy.

If there is anything we learn from basic finance, it’s that time in the market is more important than timing the market. By having a larger lump sum in the market for a longer time, you reduce sequence of returns risk.

The longer time horizon allows you to average out your investments, making it much more likely to achieve a compounded annual growth rate of 10%.

What To Invest with Interest Free Capital?

The whole idea is to invest first using future income savings, with the option to pay off the loan at any time later.

For most people, you should just invest as you normally would. If your life long strategy is to DCA into a low cost, globally diversified fund, especially using the tax efficient Irish domiciled ETFs like FWRA or ACWD or SPYL, then just invest in those.

You shouldn’t take more risk than you normally would just because it’s interest free capital. Conversely, you don’t necessarily need to take lower risk either, with one major caveat.

The only reason you would invest into lower risk vehicles (like bond funds, money market funds, or EPF self contribution) is if you aren’t sure about your future income or job security.

If you have a job heavily influenced by market spending appetite, and you have no confidence in your job security, you might be forced to sell your investments during months without balance transfer campaign offers. In that scenario, you absolutely want to make sure your capital maintains its value.

If you are highly risk averse but still want to implement this strategy, considering low risk options like bond funds, money market funds, or fixed deposits is fine. While the returns seem less exciting, it is still free money that you wouldn’t have made otherwise.

When to Avoid This Balance Transfer Strategy

While this strategy is incredibly powerful, here are a few scenarios where you should absolutely avoid it, or at least avoid utilizing your entire credit limit.

Insecure Job & Future Income

I’ve mentioned this, but it bears repeating. If your income is insecure, your priority should be securing it. If you still want to do this, stick exclusively to zero risk investments like fixed deposits. There is no guarantee that 0% interest balance transfer campaigns will always be around in Malaysia. You must have the ability to pay back those installments if the music stops.

You Plan To Apply Loan / Credit Cards in Short Term

If you are planning to apply for a mortgage or a car loan in the short term, high credit utilization on your CCRIS report may be considered a negative factor by banks, especially if you do not have a long credit history. It doesn’t mean you have to give up the strategy entirely, but consider keeping your utilization to a smaller percentage of your available limits until the loan is approved.

You Cannot Control Your Spending Habits or Stick to Plan

This strategy will backfire spectacularly if you lack discipline and give in to the temptation to spend. Remember, the idea is to front run your savings to invest, not to spend money you don’t have. It’s also a bad idea if you don’t have a clear plan on how you will invest. Figure out a 10 year portfolio plan before you execute this.

Closing Thoughts

In this post, I shared a 0 balance transfer credit card strategy that I personally exercise with no hurdles. It works for me because I have clear financial planning and intimately understand my own financial situation.

Your financial situation is different. You need to assess your own risks. I am not responsible for your financial losses, but using credit card capital responsibly to front run your portfolio is one of the most powerful levers you have as an average earner.

Anyway, welcome to leave a comment if you have any questions or want to discuss the details!

Comments